Every plastic bank card contains essential data required for its use. This includes a 16-digit card number, an expiration date, the cardholder’s name and signature, and a three-digit security code, often referred to as CVV or CVC, depending on the payment system. Let’s explore what this code is, where to find it, and when you might need it.

What is CVV?

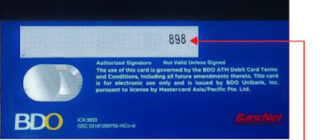

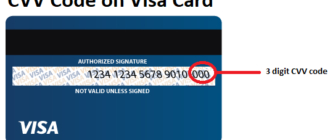

The CVV (Card Verification Value) is a three-digit security code located on the back of your bank card, next to the signature field. The name of this code can vary based on the payment system. For example, Visa and Mastercard often use terms like CVV or CVC. Variations like CVV2 or CVC2 may also appear, signifying that these codes are specifically for verifying transactions.

Each card actually has two verification codes:

- Internal Code: Stored in the card’s chip or magnetic stripe, accessible only to banking systems.

- Printed Code: Found on the back of the card, used by the cardholder for online transactions.

When discussing CVV or CVC, we generally refer to the second type, which is visible on the card.

What is the Purpose of the CVV Code?

These security codes serve as “verification codes,” providing an additional layer of protection for online payments and transfers. Their primary functions include:

- Authenticating Transactions: CVV ensures the card being used belongs to the person making the transaction.

- Enhancing Security: Just as a PIN code secures in-person transactions, the CVV code secures online payments by verifying the card’s authenticity.

For example, in physical stores or ATMs, you must enter a PIN code to complete a transaction. However, PINs cannot be used online. This is where the CVV code comes in, acting as an online equivalent of a PIN.

When Should You Share Your CVV Code?

The CVV code, like your PIN, is confidential. Only the cardholder should know this code, and it should never be shared with strangers. Sharing it puts you at risk of fraud, allowing someone to make unauthorized purchases or withdraw funds.

When you might use the CVV code:

- To complete online purchases.

- To fund an online wallet.

When you should not use or share the CVV code:

- To receive bank transfers.

- To confirm your identity during a phone call with the bank.

Remember, the CVV code is not required for any transactions outside of those mentioned above.

How to Use the CVV Code?

When shopping online, you’ll typically be directed to a secure payment page. Here, you’ll need to enter:

- Your card number.

- The expiration date.

- The cardholder’s name.

- The three-digit CVV code.

In some cases, additional security layers may be involved, such as receiving a one-time password via SMS or push notification. You’ll need to enter this password on the payment page to finalize the transaction.

Is the CVV Code Always Required?

While CVV codes are essential for most online transactions, some merchants may not require them. For example:

- Certain online stores may rely on SMS or push notifications for verification.

- Some stores may process payments with just the card number and expiration date.

This highlights the importance of safeguarding not only your CVV code but also the data displayed on the front of your card. Even partial card details can sometimes be enough for fraudulent activities.

Conclusion

The CVV code on your Visa gift card is a crucial tool for ensuring the security of your online transactions. It acts as a shield, preventing unauthorized use of your card while allowing you to shop with confidence. By understanding its purpose and following best practices for its use, you can protect your finances from fraud and enjoy a worry-free online shopping experience.