Introduction

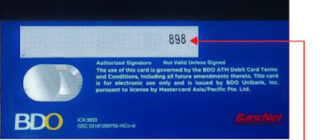

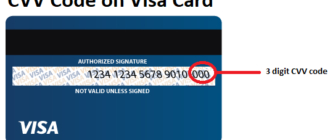

CVC codes (Card Verification Codes) are three-digit security codes found on the back of most bank cards, located near the cardholder’s signature strip. These codes are essential for securing online transactions, yet they are often misunderstood, leading to myths and misconceptions about their purpose and functionality. This article aims to debunk common myths about CVC codes and shed light on their actual role in protecting your financial data.

Myth 1: CVC Codes Can Be Used to Withdraw Cash

Reality:

CVC codes are exclusively designed for online purchases and cannot be used to withdraw cash from ATMs. ATM transactions require a separate security element—the PIN (Personal Identification Number). The CVC is intended to verify online transactions, not to authorize physical access to funds.

Myth 2: CVC Codes Can Be Used to Verify Identity

Reality:

CVC codes are not intended to serve as a form of identity verification. Banks and financial institutions rely on other methods for identity confirmation, such as phone number verification, email-based authentication, or biometric checks. The CVC is strictly used as an additional layer of security for online or phone transactions.

Myth 3: CVC Codes Can Be Shared with Third Parties

Reality:

CVC codes are confidential and should only be known to the cardholder. Sharing your CVC code with third parties can expose you to the risk of unauthorized transactions and financial loss. Even trusted individuals or entities should not be privy to this sensitive information.

Myth 4: CVC Codes Can Be Used to Restore Access to a Card

Reality:

CVC codes do not play a role in restoring access to your card. If you lose your card or need to regain access to your account, you must contact your bank and follow their reissue or recovery procedures. Banks typically use other verification processes, such as security questions, phone verification, or ID checks, to confirm your identity.

Myth 5: CVC Codes Can Be Used to Confirm Transactions Over the Phone

Reality:

Legitimate bank employees will never ask for your CVC code over the phone. If someone calls you claiming to be from your bank and requests your CVC, it is likely a scam. Banks use secure methods like OTPs (one-time passwords) or secure links to verify transactions, never the CVC.

The Real Role of CVC Codes

CVC codes are designed to enhance security during card-not-present transactions, such as online shopping or phone orders. They act as a verification tool to confirm that the person initiating the transaction has physical possession of the card. This simple but effective feature helps reduce the risk of unauthorized transactions and fraud.

Tips for Protecting Your CVC Code

- Keep It Confidential: Never share your CVC code with anyone, even if they claim to be a trusted party or organization.

- Use Secure Websites: Always ensure that the website you’re shopping on is secure (look for “https://” and a padlock symbol in the browser).

- Be Alert to Scams: Avoid providing your CVC in response to unsolicited calls, emails, or messages.

- Monitor Transactions: Regularly check your bank statements for any unauthorized activity.

- Report Lost or Stolen Cards Immediately: If your card is lost or stolen, contact your bank right away to block it and prevent misuse.

Conclusion

CVC codes are an integral part of financial security, especially for online transactions. However, they are often surrounded by myths that can lead to misuse or misunderstanding. By understanding the real purpose of CVC codes and debunking common misconceptions, you can take proactive steps to safeguard your financial data. Always stay vigilant and cautious when using your bank card, and your funds will remain secure.