Introduction

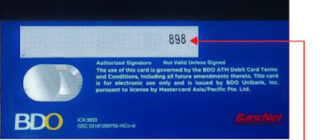

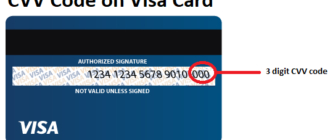

The Card Verification Value (CVV), also known as the Card Verification Code (CVC) or Card Security Code (CSC), is an essential security feature embedded in credit and debit cards. This code plays a crucial role in safeguarding transactions, particularly those conducted without the physical presence of the card, such as online or over-the-phone purchases.

Purpose of the CVV on Debit and Credit Cards

The primary purpose of the CVV is to verify that the individual making the transaction possesses the physical card. This security measure significantly reduces the risk of unauthorized use during card-not-present transactions. Merchants typically request the CVV during such transactions to confirm the authenticity of the cardholder.

Differences Between Debit and Credit Cards Regarding CVV

While both debit and credit cards employ CVVs for added security, their applications differ slightly:

- Debit Cards: The CVV on a debit card protects funds directly linked to the cardholder’s bank account. Unauthorized access to this information can lead to immediate financial loss, emphasizing the importance of safeguarding the CVV.

- Credit Cards: For credit cards, the CVV secures the cardholder’s credit line. Although fraudulent charges may not immediately affect the cardholder’s bank account, they can impact the credit limit and require resolution with the card issuer.

Advantages of the CVV

The CVV offers several benefits that enhance the security of financial transactions:

- Enhanced Security: By requiring the CVV for online and phone transactions, merchants ensure that the cardholder physically possesses the card, adding an extra layer of protection.

- Fraud Prevention: CVVs reduce the risk of fraudulent transactions, as possessing only the card number is insufficient to complete a purchase.

Disadvantages of the CVV

While the CVV is a valuable security feature, it is not without limitations:

- Limited Protection: Despite its benefits, the CVV is not foolproof. Fraudsters can still obtain the CVV through phishing scams or by physically stealing the card.

- Inconvenience for Cardholders: Cardholders must have their physical card on hand to retrieve the CVV, which can be inconvenient if the card is not readily accessible.

Tips for Protecting Your CVV

To maximize the security of your card information, follow these best practices:

- Avoid Sharing Your CVV: Never disclose your CVV to anyone, even if they claim to represent your bank or a trusted organization.

- Use Secure Websites: Only provide your CVV on websites with “https://” in the URL and a padlock icon in the address bar.

- Be Wary of Phishing Attempts: Avoid clicking on unsolicited links or providing sensitive information through emails or messages.

- Monitor Your Transactions: Regularly review your bank and credit card statements to identify and report any suspicious activity promptly.

Conclusion

The CVV is a critical element in the security infrastructure of debit and credit cards, providing an additional layer of protection against unauthorized transactions. While it is not an absolute safeguard, the CVV significantly enhances the security of card-not-present transactions, offering substantial benefits to both consumers and merchants. By understanding its purpose and adhering to best practices for its use, you can enjoy safer and more secure financial transactions.