Origins of Plastic Credit Cards

The concept of storing monetary value on physical cards revolutionized financial transactions in the mid-20th century. The idea for a multipurpose charge card emerged in 1949 when Frank McNamara envisioned a solution to carry less cash. This innovation led to the founding of Diners Club International in 1950, which introduced the first cardboard charge cards.

The transition to plastic credit cards began in 1959 when American Express released the first plastic version, followed by Diners Club in 1961. These cards quickly gained traction as they offered consumers and merchants an alternative to cash transactions.

Public Reaction and Initial Challenges

The early adoption of plastic credit cards was a mixed experience for consumers and merchants:

- Consumer Concerns:

- While many appreciated the convenience of cashless transactions, fears about overspending and debt were prevalent.

- Trust issues arose as consumers worried about fraud and misuse of their financial information.

- Merchant Difficulties:

- Merchants faced operational hurdles integrating new payment processing systems.

- The lack of standardized technology and fraud prevention measures made the transition challenging.

Technological Advancements

The success of plastic credit cards relied on overcoming these early challenges through significant technological innovations:

- Magnetic Stripe Technology:

In the early 1960s, Forrest Parry, an IBM engineer, invented the magnetic stripe, which allowed secure storage of cardholder information. This innovation enabled faster and safer transactions, laying the groundwork for widespread adoption. - Standardization Efforts:

By 1960, the American Bankers Association (ABA) initiated discussions to standardize card sizes and encoding formats. These efforts culminated in the ISO/IEC 7810 standard, ensuring compatibility across issuers and industries. - Fraud Prevention:

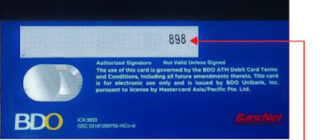

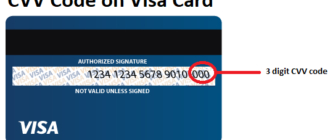

The Card Verification Code (CVC) was introduced in the late 1990s as a printed security feature to authenticate cards during remote transactions, further boosting consumer trust.

Innovations in Card Payment Systems: Tackling Challenges

Abstract:

The introduction of plastic cards required creative solutions to address integration issues, fragmented systems, and security concerns. Key developments by industry pioneers helped establish the modern card payment infrastructure.

Key Challenges in Early Adoption:

- Lack of Standardized Technologies:

- Each issuing company, such as Diners Club and American Express, relied on proprietary formats.

- Verification processes were manual, slow, and error-prone, deterring adoption.

- Fraud Risks:

- Stolen or counterfeit cards posed significant risks due to a lack of verification mechanisms.

- Transactions were vulnerable to unauthorized use, eroding trust among consumers and merchants.

- Merchant Integration:

- Without electronic card readers, merchants used impractical methods like paper slips and imprint machines, slowing transaction speeds and increasing error rates.

Pioneering Solutions to Challenges:

- Standardization of Card Formats and Technologies:

- In the 1970s, magnetic stripe technology was standardized, enabling automated data reading and verification.

- The ISO/IEC 7810 standard unified card dimensions and encoding formats, ensuring global compatibility.

- Innovations in Fraud Prevention:

- The invention of the Card Verification Code (CVC) by Mastercard in the late 1990s added an extra layer of security for card-not-present transactions.

- Authorization networks, such as BankAmericard (later Visa), enabled real-time validation of cardholder information, reducing fraudulent activity.

- Merchant Integration Technology:

- The introduction of point-of-sale (POS) terminals in the 1970s revolutionized payment processing by automating data capture and verification.

- By the 1980s, dedicated networks like VisaNet and Mastercard’s global network connected merchants and banks, streamlining transactions worldwide.

Conclusion:

The invention and evolution of plastic credit cards transformed global financial transactions. Early challenges—ranging from security risks to fragmented technologies—necessitated groundbreaking innovations, including magnetic stripes, POS terminals, and fraud prevention measures. Over time, consumer trust grew, and credit cards became a cornerstone of modern commerce, offering unmatched convenience and security.

This trajectory highlights the financial industry’s ability to adapt to emerging challenges, paving the way for future advancements in payment technologies.