Abstract

The Card Verification Value (CVV), often interchangeably referred to as the Card Verification Code (CVC), is a critical feature in modern payment systems designed to enhance security in card-not-present (CNP) transactions. This article explores the origin and meaning of CVV, examines its role in mitigating fraud, discusses potential consequences of its absence, and identifies like-minded security measures that work alongside or parallel to CVV technology.

What Is CVV?

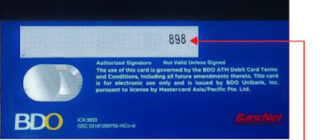

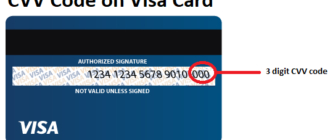

The CVV is a 3- or 4-digit code printed on payment cards, distinct from the card’s main number (PAN) and embedded data. Its primary purpose is to confirm the authenticity of a card during transactions where physical presence is not required, such as online purchases or phone orders.

- History: Introduced in the late 1990s, the CVV was developed as online and remote transactions became prevalent. Mastercard first implemented the Card Verification Code (CVC), and Visa followed with a similar feature, the CVV2.

- Functionality: The CVV ensures that the person making the transaction has access to the physical card, adding a layer of authentication beyond just the card number.

What Would Happen Without CVV?

Without the CVV or similar security features, payment systems would face significant vulnerabilities:

- Increased Fraud

- Card-not-present (CNP) transactions would become a primary target for cybercriminals. Stolen card numbers, often obtained through phishing or data breaches, could be easily exploited without requiring further verification.

- Loss of Consumer Confidence

- Frequent fraudulent transactions would erode trust in digital payment systems, leading to a potential decline in e-commerce and other card-based transactions.

- Operational Challenges for Merchants

- Merchants would face increased chargebacks due to disputed transactions, leading to financial losses and strained relationships with payment processors.

- Regulatory Implications

- In the absence of robust security measures like CVV, regulators might impose stricter requirements on merchants and financial institutions, increasing compliance costs.

Problems Solved by CVV

The CVV addresses several critical issues in modern payment systems:

- Fraud Mitigation

- By requiring the CVV for online transactions, merchants and payment processors can verify the cardholder’s possession of the card, reducing unauthorized transactions.

- Enhanced Consumer Protection

- Consumers are less likely to face unauthorized charges, and in cases where fraud does occur, liability protections often shield them from financial loss.

- Global Standards and Interoperability

- The CVV has become a universal standard in the payments industry, streamlining security protocols across regions and networks.

- Simplification of Merchant Operations

- The use of CVV reduces the risk of chargebacks and disputes, simplifying transaction processing and increasing merchant confidence in accepting card payments.

Like-Minded Projects and Technologies

Several other security measures and technologies work alongside or share similar objectives with CVV to enhance payment security:

- 3D Secure Protocols (e.g., Verified by Visa, Mastercard SecureCode)

- These protocols add an additional layer of authentication by redirecting users to their card issuer’s secure page during a transaction. Users verify their identity through a one-time password (OTP) or other means.

- Dynamic CVV

- Emerging technologies are introducing CVVs that change periodically, displayed on a small electronic screen on the card. This dynamic feature significantly reduces the risk of static code exploitation.

- Tokenization

- Instead of transmitting actual card data, tokens are used in transactions. These unique identifiers are useless if intercepted, adding a robust layer of protection.

- Biometric Authentication

- Fingerprint scans, facial recognition, or voice verification are being integrated into payment systems for enhanced user authentication.

Collaborative Efforts in Payment Security

Organizations and industry groups contribute to payment security standards alongside CVV implementation:

- PCI Security Standards Council

- Develops and enforces standards like PCI DSS (Payment Card Industry Data Security Standard), ensuring secure handling of cardholder data.

- EMVCo

- Oversees EMV chip card standards, reducing fraud in card-present transactions and complementing CVV in card-not-present scenarios.

- Financial Institutions and Payment Networks

- Banks and payment networks like Visa, Mastercard, and American Express collaborate on shared security frameworks, including CVV and additional layers of protection.

Conclusion

The CVV is a cornerstone of modern payment security, safeguarding billions of card-not-present transactions annually. Without this feature, the payment ecosystem would be far more vulnerable to fraud, resulting in significant financial and reputational risks. By integrating CVV with complementary technologies and protocols, the financial industry continues to innovate and protect against emerging threats, ensuring the trust and growth of digital payments worldwide.