The concept of storing monetary value on plastic cards, commonly known as credit cards, emerged in the mid-20th century and revolutionized financial transactions.

Origins of the Plastic Credit Card

The idea of a multipurpose charge card was conceived in 1949 by Frank McNamara, who founded Diners Club International in 1950. Initially, Diners Club cards were made of cardboard. The transition to plastic cards began in 1959 when American Express introduced the first plastic credit card, followed by Diners Club in 1961.

Public Reaction and Initial Challenges

The introduction of plastic credit cards was met with both enthusiasm and skepticism. Consumers appreciated the convenience of cashless transactions, but concerns about overspending and debt arose. Merchants faced challenges integrating new payment systems and ensuring transaction security. The lack of standardized technology and fraud prevention measures further complicated early adoption.

Technological Advancements

To address security concerns, IBM engineer Forrest Parry developed the magnetic stripe technology in the early 1960s, allowing secure storage of cardholder information. This innovation facilitated widespread acceptance of plastic credit cards by enhancing transaction security and efficiency.

Conclusion

The development of plastic credit cards transformed financial transactions, offering unprecedented convenience. Despite initial challenges, technological advancements and evolving consumer trust established credit cards as a fundamental component of modern commerce.

Innovations in Card Payment Systems: Early Solutions to Integration and Security Challenges

Abstract

The introduction of plastic payment cards in the mid-20th century presented significant challenges to adoption, including the lack of standardized technologies, difficulties in integrating new payment systems, and concerns about transaction security. This article explores the early efforts by industry pioneers to address these issues, focusing on technological innovations, regulatory measures, and collaborative initiatives that laid the groundwork for the modern card payment infrastructure.

Introduction

The emergence of payment cards in the 1950s and 1960s marked a transformative shift in commerce. Despite their promise of convenience, early cards were hampered by technological and operational obstacles. Merchants struggled to accept cards due to the lack of standardized payment processing systems, while consumers and financial institutions grappled with concerns about fraud and secure transactions. These barriers necessitated creative solutions to ensure the viability of card-based payments.

Early Challenges

- Lack of Standardized Technologies

- Payment systems in the 1950s were fragmented. Each issuing company (e.g., Diners Club, American Express) used proprietary formats, creating interoperability issues.

- Manual verification of cardholder creditworthiness was time-consuming and error-prone, further deterring adoption.

- Fraud Prevention

- The absence of fraud prevention mechanisms made card transactions risky for merchants and consumers.

- Stolen or counterfeit cards could easily be used without verification, eroding trust in the system.

- Merchant Integration

- Early card readers were non-existent. Merchants relied on impractical methods such as paper slips and imprint machines, which slowed transactions and increased errors.

Pioneering Solutions

- Standardization Efforts

- In 1960, the American Bankers Association (ABA) led discussions to standardize card dimensions and data encoding. This effort culminated in the ISO/IEC 7810 standard, which established a uniform size and shape for cards globally.

- Collaboration between banks and card issuers helped introduce standardized magnetic stripe technology in the 1970s, developed by IBM engineer Forrest Parry. The stripe stored essential cardholder data, enabling automated transactions.

- Innovations in Fraud Prevention

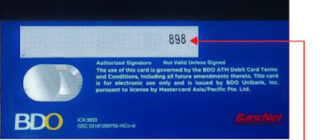

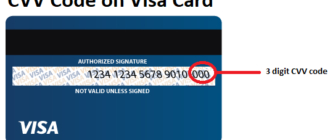

- The invention of the Card Verification Code (CVC) in the late 1990s was a pivotal step. Pioneered by Mastercard, the CVC added a printed security feature to verify the card’s legitimacy during remote transactions.

- Early adoption of authorization networks (e.g., BankAmericard, which later became Visa) in the 1960s and 1970s enabled real-time validation of cardholder data, reducing the risk of fraudulent transactions.

- Merchant Technology

- The introduction of point-of-sale (POS) terminals in the 1970s revolutionized merchant integration. These devices automated the process of reading magnetic stripes, verifying transactions, and generating receipts.

- By the 1980s, companies like Visa and Mastercard developed dedicated networks (e.g., VisaNet), connecting merchants and banks globally for seamless transaction processing.

Collaborative Industry Efforts

- Formation of Card Networks

- In 1966, the Interbank Card Association (now Mastercard) was established, promoting collaboration among banks to create a unified payment system.

- VisaNet, launched by Visa in 1973, became the first electronic authorization and settlement system, addressing inefficiencies in manual processing.

- Government and Regulatory Involvement

- Governments introduced consumer protection laws to encourage card usage. The Truth in Lending Act (1968) in the United States mandated clear disclosure of credit terms.

- The PCI DSS (Payment Card Industry Data Security Standard) was later introduced to enhance security across card networks.

Results and Long-Term Impact

The combined efforts of innovators, regulatory bodies, and collaborative networks led to the widespread adoption of payment cards by the late 20th century. The introduction of technologies like magnetic stripes, electronic authorization, and secure networks significantly mitigated fraud risks and operational inefficiencies. These advancements paved the way for modern solutions such as chip cards, contactless payments, and digital wallets.

Conclusion

The early challenges faced by the payment card industry underscored the importance of standardization, technological innovation, and collaboration. By addressing integration and security concerns, industry pioneers not only overcame initial resistance but also laid the foundation for the global payment systems we rely on today. These efforts demonstrate the critical role of adaptability and cooperation in overcoming technological disruptions.

References

- “The History of Credit Cards.” Time Magazine, 2023.

- Parry, Forrest. “Development of Magnetic Stripe Technology.” IBM Archives, 1972.

- “PCI DSS: The Evolution of Payment Security Standards.” PCI Security Standards Council, 2006.