Introduction

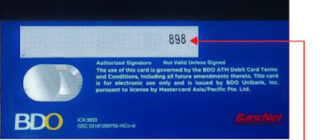

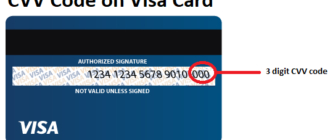

The Card Verification Value (CVV), also referred to as the Card Security Code (CSC), is a pivotal security feature designed to enhance the safety of card-not-present transactions, such as online and phone purchases. This three- or four-digit number, printed on credit and debit cards but not stored in their magnetic stripe or chip, provides an additional layer of verification. It ensures that only the cardholder can authorize a transaction. While CVV codes have become standard in many developed countries, their implementation in developing nations presents unique challenges and opportunities.

What is a CVV Code?

The CVV code is a key element in preventing fraud, especially in online transactions. By requiring this code, merchants ensure that the individual making a purchase has physical possession of the card. This measure significantly reduces the risk of unauthorized transactions and reinforces consumer trust in digital payment systems.

Implementation of CVV in Developing Countries

1. Financial Infrastructure Development

One of the primary factors affecting the adoption of CVV codes in developing regions is the maturity of financial systems.

- Challenges: Limited banking infrastructure, low penetration of electronic payment systems, and widespread reliance on cash hinder the seamless integration of CVV codes.

- Opportunities: As developing countries work to modernize their financial infrastructure, CVV codes can serve as a foundational security feature in emerging digital payment systems.

2. Regulatory Frameworks

Strong and enforceable regulations governing electronic transactions are critical for the successful implementation of CVV codes.

- Challenges: In many developing nations, regulatory frameworks are still evolving, leading to inconsistent application of security measures.

- Progress: Efforts by governments and financial institutions to introduce standardized regulations are gradually improving the adoption and enforcement of CVV codes.

3. Technological Adoption

The pace of technological adoption directly impacts the deployment of CVV codes.

- Barriers: Low digital literacy, limited smartphone penetration, and unreliable internet connectivity slow the progress of secure digital transactions.

- Solutions: Targeted initiatives to improve access to technology and digital education can accelerate the use of secure payment features like CVV codes.

Perception and Effectiveness

1. Consumer Awareness

A lack of awareness about CVV codes often results in underutilization and security vulnerabilities.

- Many consumers are unfamiliar with the purpose of CVV codes and their role in preventing fraud.

- Education campaigns by banks and governments are essential to bridge this knowledge gap.

2. Trust in Digital Transactions

Concerns about fraud and misuse deter many consumers from embracing digital payments.

- Preference for Cash: Due to limited understanding of security features, cash transactions remain the default choice for many in developing regions.

- Building Confidence: Demonstrating the effectiveness of CVV codes through educational initiatives and secure payment platforms can build trust in digital transactions.

Development Timeline of CVV Implementation

1. Initial Introduction

After the global rollout of CVV codes in the late 1990s, many developing countries began incorporating this feature as part of broader financial reforms.

2. Progressive Implementation

Over the past two decades, as digital payment systems have gained traction, the use of CVV codes has expanded.

- Improved financial systems and increased adoption of smartphones and internet services have facilitated this growth.

3. Ongoing Challenges

Despite progress, significant challenges remain:

- Limited Banking Access: Many rural areas still lack adequate banking services.

- Technological Barriers: Poor infrastructure and low digital literacy continue to impede adoption.

- Regulatory Hurdles: Inconsistent enforcement of security standards undermines efforts to integrate CVV codes fully.

Conclusion

The adoption of CVV codes in developing countries is a critical step towards enhancing transaction security and fostering trust in digital payment systems. However, its implementation is influenced by several factors:

- The development of financial infrastructure,

- The establishment of robust regulatory frameworks,

- And the adoption of relevant technologies.

To maximize the effectiveness of CVV codes:

- Governments and financial institutions must invest in financial inclusion programs.

- Comprehensive digital literacy campaigns should be conducted to educate consumers on secure payment practices.

- Collaborative efforts to strengthen the regulatory environment are essential for ensuring long-term success.

By addressing these challenges, developing countries can leverage CVV codes as a vital tool in their journey towards secure, inclusive, and efficient digital economies.